Australian Alternative Energy Forum

Not Really a Forum, more of my memory aid.

Comments on this forum should never be taken as investment advice.

|

|||||||

|

|

|

Thread Tools | Display Modes |

|

#1

07-18-2011, 03:55 AM

07-18-2011, 03:55 AM

|

|||

|

|||

|

It seems that many have misunderstood the ramifications of China's announcement re the new export quota for 2011 2H... In a nutshell by including for the first time ferrous alloys (dysprosium ferro alloy, terbium ferroalloy etc.) which contain more than 10% rare earths in the quota the yearly allowance is around 28,200t down from the 2010 allowance of 30,260t.

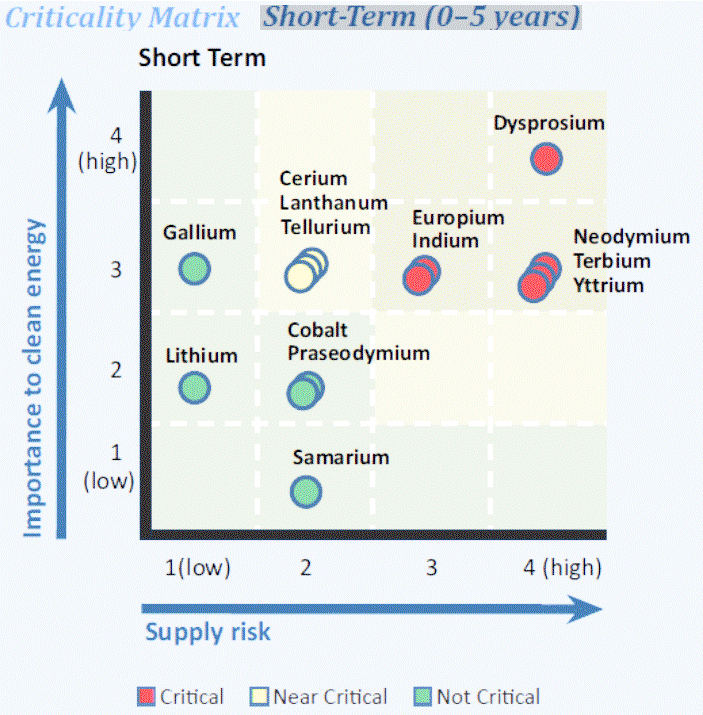

This 7% reduction in the face of increasing demand combined with the recent reduction in LYC's share price points to a buying opportunity as LYC will be the first new non-China based supplier. One well respected broker has LYC as a buy with a price target of $2.60 predicated on a REE basket price of US$30/Kg until 2015 when competing supply will come on-stream. As today's REE basket price is ~ US$225 per kg there seems to be plenty of upside to that particular forecast... As Alkane will also soon be in production it may be worthwhile to grab a few sooner than later. Short term, 0 - 5 years, Criticality Matrix for Green Technology Substrates (US Department of Energy 2010)  (I hold LYC, ALK, GGG and KRB)

Disclaimer: The author of this post, may or may not be a shareholder of any of the companies mentioned in this column. No company mentioned has sponsored or paid for this content. Comments on this forum should never be taken as investment advice.

|

|

#2

07-19-2011, 01:29 PM

|

|||

|

|||

|

Disclaimer: The author of this post, may or may not be a shareholder of any of the companies mentioned in this column. No company mentioned has sponsored or paid for this content. Comments on this forum should never be taken as investment advice.

|

|

«

Previous Thread

|

Next Thread

»

Linear Mode

Linear Mode

|

|

All times are GMT. The time now is 10:27 AM.